In the October blog post Universal health care, I wrote about how everyone in France must have health insurance. We had received our Carte Vitale, the ID card to show that we are part of the French healthcare system, that we present at the doctor’s office, hospital, laboratory, pharmacy, etc. Coverage is generally 70 percent of the cost of the procedure leaving the patient to pay the remaining 30 percent out of pocket or to buy a private top-up insurance policy that costs between 50 and 100 euros per month per person. Coverage for dental, vision, and hearing problems will increase to 100 percent within 2 years. Anyone who has a long term disease such as cancer or diabetes is already covered at 100 percent as are people who are unable to afford additional insurance. We’ve now signed up for assurance maladie complémentaire more commonly called a mutuelle.

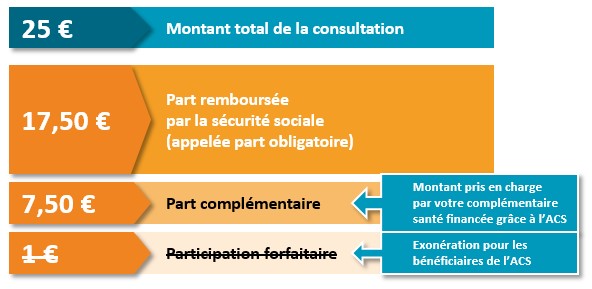

Whether to buy that top-up insurance was a question for us. I read a summary of a 5-year study conducted by a university in Paris that followed young people, families, and retired adults to compare costs. The retired couples ended up breaking even; that is, their expenditures were the same whether they paid for additional insurance to cover the 30 percent unreimbursed charges or simply paid out-of-pocket for any medical services they needed. A routine visit to the doctor costs 25 euros, of which the patient pays 7.50 euros. I saw that an emergency room visit for a broken finger that involved the doctor’s time plus x-rays left 29 euros unpaid while someone else had a knee replacement and had to come up with 1000 euros at the end of his hospital stay. Since mutuelles come in a wide range of options with a variety of prices to match, one that would come into effect for a hospital stay but leave us to pay for our own annual doctor’s visit might be wise.

For people who cannot afford to pay for additional insurance, the government provides a supplement to cover most or all of the extra costs which is explained on the ACS website https://www.info-acs.fr/index.php. That’s where we saw a list of the 687 companies that sell mutuelles. No wonder we were having difficulty in deciding who to go with since there were hundreds of choices. That site did give us a good starting point because it showed that a retired couple is allowed 1100 euros per year to purchase one of three levels of coverage in a good-better-best scenario. At least we now knew that for 92 euros per month, a couple should be able to buy basic top-up insurance to avoid additional out-of-pocket charges.

There are several for-profit insurance comparison websites and we did use one that advertises heavily on TV to begin our search. It was easy to use and lets you change your profile at will to see the impact of adding dental or decreasing reimbursements for a private room for example. They can only search, of course, the companies with which they are affiliated, so we needed more.

To continue narrowing down our choices we signed up for a month with Que Choisir, a subscriber-supported service very similar to Consumer Reports in the US, that allows you compare companies on price and 7 other criteria. We found the categories of “Value For Money” and “Adequacy for Failing Health” to be especially helpful. For each offer that looks attractive, you can click on the company name to find out more information. Armed with that we were ready for the next step.

From that comparison website we went directly to our chosen insurer’s site to confirm the details we had just seen and to sign up, pay, and receive a confirmation online all within a few minutes. We have decided initially to go with a mutuelle that has good hospitalization top-up but little else since we could upgrade instantly should we want to add dental, glasses, hearing aids, etc. The cost is 37 euros per month for the two of us combined. We find that to be pretty inexpensive peace of mind.

Que Choisir is 6.99 a month: https://www.quechoisir.org/

Update, June 2023: I just read a tip on how to calculate the monthly cost per couple of a middle-of-the-road mutuelle; that is, one that covers much more than our hospital-only plan but might not reimburse you in-full for all the procedures covered. Simply add the ages of the two partners together and the result will be an approximation of the monthly cost. For example, if one person is 63 and the other 65 then the total (63 + 65 = 128) would be 128 euros. By the way, our mutuelle that began at 37 euros per month is now 48 euros per month, five years later.

What a comprehensive, useful post explaining the minefield of mutuelles! This will be helpful to a lot of people.

LikeLiked by 2 people

As always, great info…thanks for the link to quechosir….I’ve been looking for a CR replacement. This year, I got a Mutuelle with my insurance company because I knew them, they speak English, and for me, the best option. Now I will start investigating for next year. Have you kept your Medicare? I’ve cancelled the prescription and the supplement and can’t decide about the other.

LikeLiked by 1 person